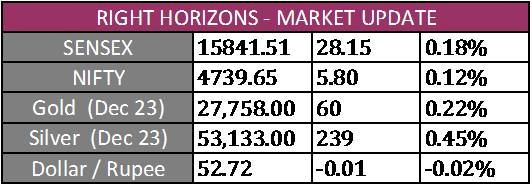

Indian Markets

Positive global cues have helped the main Indian stock indices open with a positive bias on the last trading session of what has been a tumultuous year for the domestic markets.

However, there is no certainty on whether the early morning gains could be sustained throughout the day as most of the headwinds that weighed on the markets have not been dealt with completely. Investors will continue to be cautious in the early part of 2012.

The outcome of state elections in Uttar Pradesh could have a significant bearing on policy formulations by UPA II, including the Union Budget. It might also change some political and strategic equations at the Centre. So, all eyes will be fixed on the UP elections in the days and weeks to come.

Talking of politics, USA, the world's largest economy, will also hold Presidential elections later in 2012. A leadership change is also in the offing in China. Elections are scheduled in Russia, Iran, Egypt, France, Greece and South Korea among others.

The Lokpal Bill could not clear the Rajya Sabha due to resistance from several parties, including Trinamool Congress. The passage of the Bill will be in a limbo till the next session. The Lok Sabha was adjourned sine die while the Rajya Sabha ended abruptly at the stroke of midnight without the House taking a vote on the Lokpal Bill.

State-run oil companies are mulling a hike in petrol prices. The proposed move may still be nixed by the Government in view of the upcoming state polls.

US and European Markets

U.S. stocks rose on Thursday in a thinly-traded session as investors focused on signs of strength in the economy before calling it a year. Dow Jones rose 136 points, or 1.1%, to end at 12,287. S&P 500 added 13 points, or 1.1%, to 1,263. Nasdaq gained 24 points, or 0.9%, to 2,614.

European stock markets closed higher Thursday in thin trading conditions, helped by gains for Wall Street and after an Italian debt auction was taken in stride. Britain's FTSE 100 added 0.8%, DAX in Germany rose 0.9% and France's CAC 40 rose 1.1%.

Asian Markets

Today all the Asian indices are trading in the green except Strit Times, which is down by 0.3%. Shanghai and Hang Seng are trading higher by 1% and 0.4% respectively. Nikkei and Taiwan are up 0.3% and 0.1% respectively. SGX Nifty is trading higher by 36.5 points.

Currencies

The Indian rupee ended steady on Thursday vs the Dollar, recovering from the day's lows on suspected central bank intervention and dollar-selling by nationalised banks for a second day in a row.

Commodities

Among the metals, Nickel and Copper lost 2.5% and 1.9% respectively. Zinc and Aluminium fell by 0.5% and 0.4% respectively. Oil for February delivery rose 31 cents to $99.05 a barrel. Gold futures for February delivery fell $23.20 to $1,540.90 an ounce. Gold prices have softened due to a stronger dollar.

Key events to watch for today

India - CPI Industrial Workers data

US - Fed Balance Sheet

China - PMI Manufacturing Index

Italy - PPI data

Outlook

Today, the Indian market is likely to open in the green following strong global cues and could trade in a range through the day. Support on Nifty is at 4,600-4,540 while resistance is at 4,720-4,800. Among the sectoral indices, Auto stocks could outperform while Metal stocks look weak.

Sources- RH Morning data, HDFC SEC